A balance for a permanent account carries over from period to period and represents worth at a specific point in time. For small and large businesses alike, temporary accounts help accounting professionals track economic activity, manage company finances, and establish a clear record of profit and loss. A software company hires a marketing agency on a six-month contract, agreeing to pay the agency $30,000 at the end of the contract period. At the end of the contract, the software company is obligated to pay the marketing agency. This would be classified as accounts payable, a financial obligation from services rendered on credit.

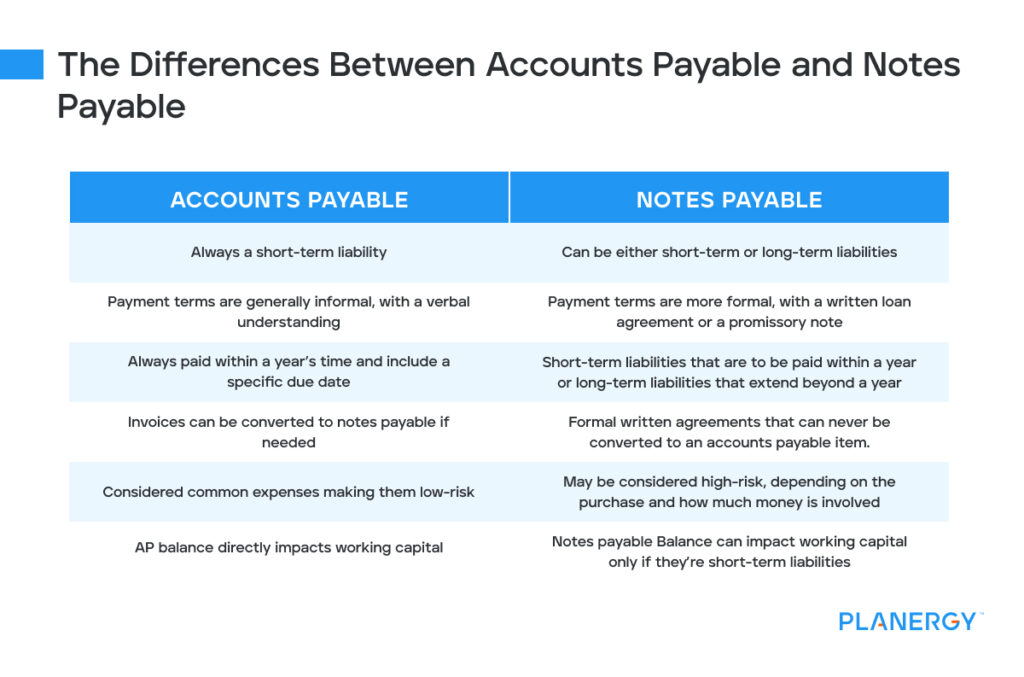

Accounts Payable Vs. Notes Payable: Differences & Examples

A zero-interest-bearing note (also known as non-interest bearing note) is a promissory note on which the interest rate is not explicitly stated. When a zero-interest-bearing note is issued, the lender lends to the borrower an amount less than the face value of the note. At maturity, the borrower repays to lender the amount equal to is notes payable a permanent or temporary account face vale of the note. Thus, the difference between the face value of the note and the amount lent to the borrower represents the interest charged by the lender. Closing entries are taught in accounting classes to help students understand the accounting process and how financial information moves through the accounting software.

An indicator of ongoing progress vs. an indicator for a discrete time period

In contrast, temporary accounts provide a view of financial activities within a specific timeframe. An account with a balance that is the opposite of the normal balance. For example, Accumulated Depreciation is a contra asset account, because its credit balance is contra to the debit balance for an asset account.

Revenue accounts

Read our articles about How to calculate operating cash flow and Ecommcer business insurance. Whether you’re just starting your business or you’re already well on your way, keeping organized financial records is a must. Download our FREE whitepaper, How to Set up Your Accounting Books for the First Time, for the scoop.

How Can HighRadius Enhance the Management of Temporary and Permanent Accounts?

Temporary vs. permanent accounts, both are crucial components of the accounting process, serving different purposes in the creation of a company’s financial statements. An accountant doesn’t choose between them but uses them both as needed based on the nature of the business transactions they’re recording. Permanent accounts are accounts that you don’t close at the end of your accounting period. Instead of closing entries, you carry over your permanent account balances from period to period. Basically, permanent accounts will maintain a cumulative balance that will carry over each period.

How Can Accounts Receivable Automation Help?

Because you did not close your balance at the end of 2021, your sales at the end of 2022 would appear to be $120,000 instead of $70,000 for 2022. An allowance granted to a customer who had purchased merchandise with a pricing error or other problem not involving the return of goods. If the customer purchased on credit, a sales allowance will involve a debit to Sales Allowances and a credit to Accounts Receivable. Here are some examples with journal entries involving various face value, or stated rates, compared to market rates. In the following example, a company issues a 60-day, 12% discounted note for $1,000 to a bank on January 1. In the following example, a company issues a 60-day, 12% interest-bearing note for $1,000 to a bank on January 1.

- Permanent accounts encompass all accounts consolidated in the balance sheet.

- Temporary accounts are closed out (returned to a zero balance) each month to prepare the accounts to accumulate the next month’s revenues and expenses.

- Instead, they carry their balances forward, continuously accumulating data over time.

In accounting, being able to run reports based on a time period is critical for understanding the relationship between revenue and expenses. Permanent accounts represent what a business owns and what a business owes. An example of this in personal finance would be the ownership of a house (an asset), the mortgage on that house (a liability), and the difference between the two (asset minus liability) is equity. The value of the house and the balance of the mortgage impact multiple accounting periods (months and years). The income statement, which shows the profitability of a company during a particular period, is primarily derived from the revenue and expense accounts.

In a business, the assets, liabilities, and equity accounts will be tracked over the life of the business. Transactions may sometimes seem to blur the lines between categories. For instance, a long-term prepaid expense might feel like an asset, but it’s typically recorded in a temporary account due to the eventual recognition of the expense. In such cases, generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS) provide guidelines for categorization.

Accountants then prepare financial documents to show that this took place. This is in contrast to temporary accounts (like revenue, expense, and dividend accounts), which are cleared to Retained Earnings at the end of each accounting period. The choice between temporary and permanent accounts is not a matter of preference—it’s determined by the nature of the transaction. Misclassifying transactions can lead to inaccurate financial reports, which can mislead decision-makers and potentially violate regulatory standards. On a border note, HighRadius offers a cloud-based solution that helps accounting professionals streamline and automate the financial close process for businesses. We have helped accounting teams from around the globe with month-end closing, reconciliations, journal entry management, intercompany accounting, and financial reporting.

This is an owner’s equity account and as such you would expect a credit balance. Other examples include (1) the allowance for doubtful accounts, (2) discount on bonds payable, (3) sales returns and allowances, and (4) sales discounts. For example net sales is gross sales minus the sales returns, the sales allowances, and the sales discounts.

Although permanent accounts are not closed at year-end, businesses must carefully review transactions annually, ensuring that only the proper items are recorded. Plus, since having too many permanent accounts can increase and complicate accounting workloads, it can be helpful for companies to assess whether some of these accounts can be combined. A retail store orders and receives $10,000 of merchandise from a supplier. The supplier offers 30-day payment terms, which means the retail store has 30 days to pay the outstanding amount.